Inflation Meets Estimates, Home Sales Stall Week of February 24, 2025 in Review The Federal…

Real Estate Week in Review for May 20, 2024

April brought cooler than forecasted consumer inflation, which was welcome news after the first quarter’s more persistent readings. Meanwhile, confidence among home builders declined and new construction activity was softer than expected. Read on for these stories and more:

-Friendly Consumer Inflation Number

-Revisions the Real Story on Wholesale Inflation

-Home Builder Sentiment Hammered Lower

-Housing Starts, Permits Lower Than Expected

-Flat Retail Sales Start of a Slowdown?

-Watching Trends in Jobless Claims

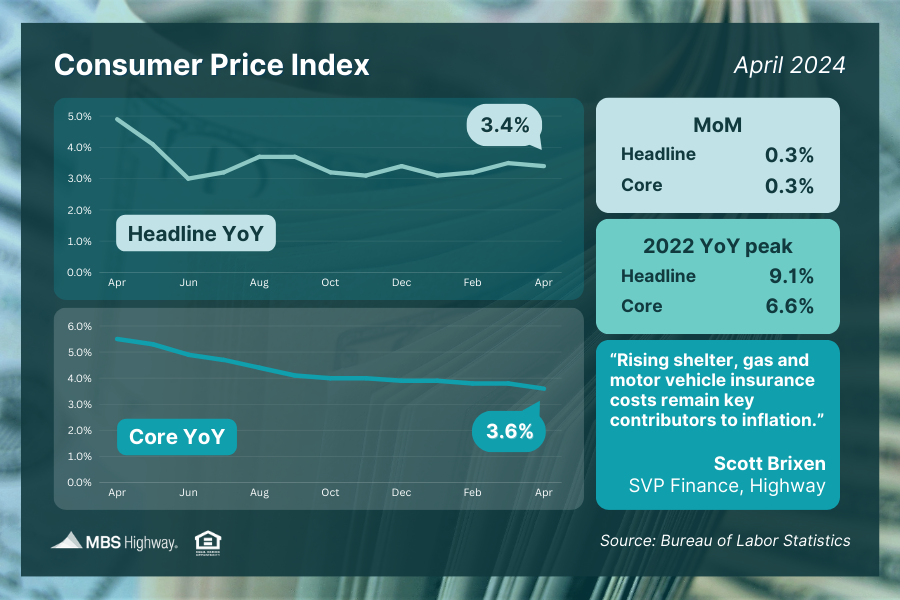

Friendly Consumer Inflation Number

The latest Consumer Price Index (CPI) showed cooler than expected inflation in April, with the headline reading up 0.3% from March versus the forecasted 0.4% rise. On an annual basis, CPI eased from 3.5% to 3.4%, which was a move lower in the right direction following the uptick in March. The Core measure, which strips out volatile food and energy prices, increased 0.3% while that annual reading declined from 3.8% to 3.6%.

Rising shelter, gas and motor vehicle insurance costs were key reasons for the pricing pressure that was seen last month.

What’s the bottom line? The Fed has been working hard to tame inflation, hiking its benchmark Fed Funds Rate (which is the overnight borrowing rate for banks) eleven times between March 2022 and July 2023. These hikes were designed to slow the economy by making borrowing more expensive, so the demand for goods would be lowered, thereby reducing pricing pressure and inflation.

While inflation was making good progress lower late last year, readings throughout the first quarter of this year were unexpectedly high, causing the Fed to hold the Fed Funds Rate steady as they take a more patient approach to cuts than initially thought. April’s cooler than expected readings were a welcome sign that inflationary pressures may continue to ease as we move further into the year.

Revisions the Real Story on Wholesale Inflation

The Producer Price Index (PPI), which measures inflation on the wholesale level, rose 0.5% in April, coming in hotter than estimates. Core PPI, which strips out volatile food and energy prices, was also above forecasts at a 0.5% rise.

What’s the bottom line? On the surface, these monthly figures looked like a significant rise in monthly wholesale inflation, but a deeper dive into the data tells a different story. Revisions to the previous report for March showed inflation was tamer than initially reported for that month, with both the headline and core readings revised lower from 0.2% to -0.1%. That’s a huge difference!

Plus, the year-over-year figures (2.2% headline and 2.4% core) came in as expected and in line with what the Fed wants to see, meaning the report wasn’t as concerning as the headline figures suggested.

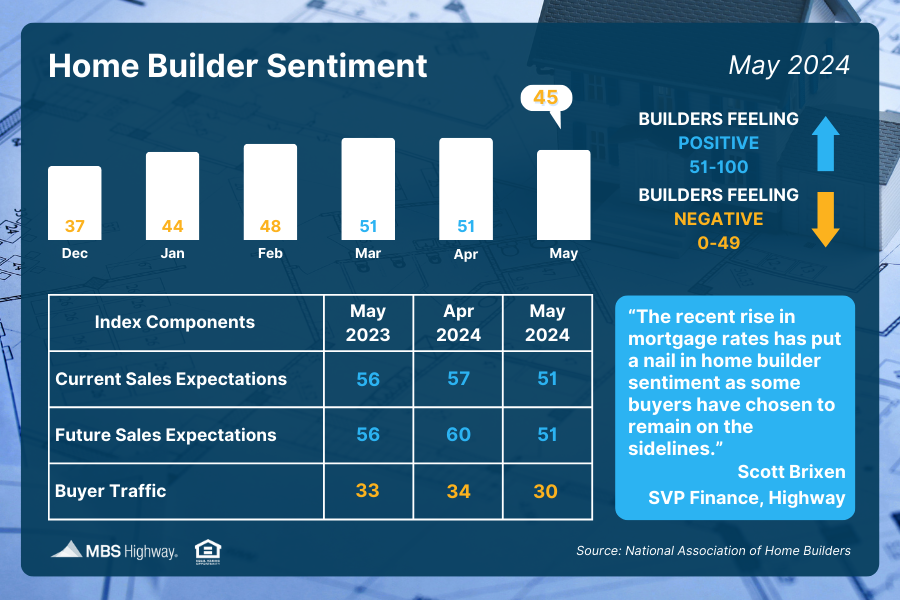

Home Builder Sentiment Hammered Lower

Confidence among home builders fell back below the key breakeven threshold of 50, per the National Association of Home Builders (NAHB), as their Housing Market Index dropped six points to 45 in May. Any score over 50 on this index, which runs from 0 to 100, signals that more builders view conditions as good than poor.

Among the three index components, current and future sales expectations both remain in expansion territory, but they fell sharply from April. The gauge judging buyer traffic also declined, remaining in contraction territory.

What’s the bottom line? NAHB’s Chair, Caril Harris, explained, “The market has slowed down since mortgage rates increased and this has pushed many potential buyers back to the sidelines.” He added that builders are concerned about some recent code rules that could lead to increased costs, which also impacted sentiment overall.

Housing Starts, Permits Lower Than Expected

Housing Starts rebounded in April, rising 5.7% from March, though coming in lower than economists had forecasted. However, starts for single-family homes, which make up the bulk of homebuilding and are the most crucial due to buyer demand, were essentially flat at a 0.4% decline. There was a similar trend in future construction, with Building Permits moving lower despite much needed supply.

What’s the bottom line? While Housing Completions did rise in April, softer than expected construction activity this spring could limit much needed supply down the road. This bodes well for appreciation and shows that opportunities remain to build wealth through homeownership.

Flat Retail Sales Start of a Slowdown?

There are signs that consumers are reining in their spending, as Retail Sales were unchanged from March to April. Sales in March were also revised downward from the originally reported 0.7% gain to a 0.6% gain when compared to February.

What’s the bottom line? The pause in spending last month was a miss on estimates, as forecasters had predicted a 0.4% gain. But with credit card balances reaching $1.12 trillion at the end of the first quarter (per the New York Fed’s Quarterly Report on Household Debt and Credit) and pandemic-era savings fully spent as of March 2024 per San Francisco Fed analysts, a slowdown in discretionary spending is also not surprising.

The Fed will be closely watching future Retail Sales reports, as the strength of our economy will also impact their monetary policy decisions this year.

Watching Trends in Jobless Claims

Initial Jobless Claims fell by 10,000 in the latest week as 222,000 people filed for unemployment benefits for the first time. Continuing Claims rose 13,000, with 1.794 million people still receiving benefits after filing their initial claim.

What’s the bottom line? While Initial Jobless Claims declined from the previous week, they remain in breakout territory above the low levels that were recently reported (ranging from 208,000 to 213,000 in nine of the ten weeks before these last two reports). Continuing Claims are also still trending near some of the hottest levels we’ve seen in recent years.

This data follows other recent reports that suggest softening in the labor sector, such as weaker than expected job growth in April, declining job openings, and the low quit rate. If softer employment data continues, this could pressure the Fed to cut the Fed Funds Rate, given their dual mandate of price stability and maximum employment.

Family Hack of the Week

Get ready for barbecue season with this easy and delicious recipe for Grilled Vegetables courtesy of the Food Network. Yields 6 servings.

Place a grill pan over medium high heat or turn on your barbecue to medium-high. Cut 3 red bell peppers in half. Gather 3 yellow squash, 3 zucchini, and 3 Japanese eggplant and slice them lengthwise into 1/2-inch-thick rectangles. Trim 1 pound of asparagus, cut the roots off 12 green onions, and clean 12 cremini mushrooms.

Add vegetables to a large dish and brush with 1/4 cup olive oil to coat and season with salt and pepper. Grill the vegetables until tender and lightly charred, about 8 to 10 minutes for the bell peppers; 7 minutes for the squash, zucchini, eggplant, and mushrooms; and 4 minutes for the asparagus and onions.

Arrange the vegetables on a platter and drizzle with an herb mixture of 2 tablespoons olive oil, 3 tablespoons balsamic vinegar, 2 cloves minced garlic, 1 teaspoon chopped Italian parsley, 1 teaspoon chopped basil, 1/2 teaspoon chopped rosemary, and salt and pepper to taste.

What to Look for This Week

Housing highlights include April’s Existing Home Sales on Wednesday and New Home Sales on Thursday. The latest Jobless Claims will also be reported on Thursday.

Plus, the minutes from the Fed’s latest meeting will be released on Wednesday and a parade of Fed speakers throughout the week always has the potential to move the markets.

Technical Picture

After a nice rally over the last few weeks, Mortgage Bonds have fallen below their 100-day Moving Average and ended the week testing the 100.42 Fibonacci level. The 10-year ended last week back up around 4.42%, testing the dual ceiling comprised of its 50-day Moving Average and the 4.418% Fibonacci level.

Related Posts