Week of August 12, 2024 in Review

Inflation made important progress lower in July while homebuilder confidence and new construction slowed. Read on for these stories and more:

-Consumer Inflation Falls Below Key Milestone

-Wholesale Inflation Cooperates with Cool Reading

-Home Builders Have Mixed Emotions

-Housing Starts Slowed, Signaling a Tight Inventory Picture Ahead

-Retail Sales Hotter for the Summer

-Jobless Claims Dip Lower

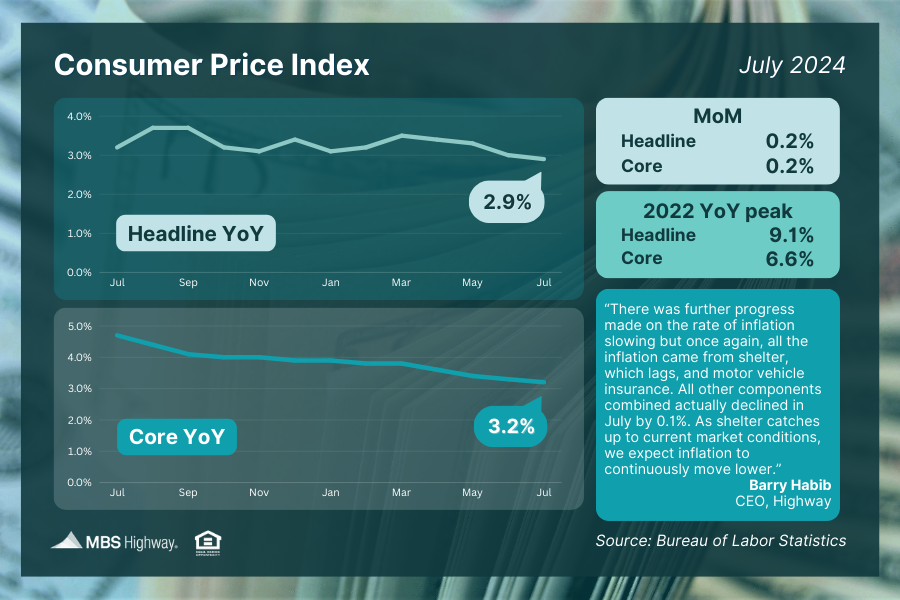

Consumer Inflation Falls Below Key Milestone

The latest Consumer Price Index (CPI) showed more progress on inflation, as consumer prices rose 2.9% for the 12 months ending in July. This marked a slowing from June’s 3% annual gain and the first time CPI fell below 3% since March 2021. The Core measure, which strips out volatile food and energy prices, increased 0.2% from June while the annual reading declined from 3.3% to 3.2%.

Shelter and motor vehicle insurance costs were key reasons for the pricing pressure that was seen last month, with the shelter component driving 90% of the monthly increase in the all items index, per the Bureau of Labor Statistics. Many other major items (such as energy, new/used cars, and airline fares) actually saw prices flat to down in July. This suggests that most of inflation has been quelled except for a few key areas that are keeping it artificially high.

What’s the bottom line? Cooling consumer inflation combined with signs that the economy and job market are slowing have led to growing calls for the Fed to begin cutting their benchmark Fed Funds Rate, which is the overnight borrowing rate for banks.

Currently, there are near certain odds that the Fed will cut rates at their next meeting on September 18, though additional reports released between now and then will play a pivotal role in this decision. On the inflation front, Fed members will want to see continued progress lower in the next Personal Consumption Expenditures (August 30) and Consumer Price Index (September 11).

The Fed will also closely dissect the August Jobs Report (September 6) for further signs of labor sector weakness or rising unemployment, which could also impact the size of a potential cut.

Wholesale Inflation Cooperates with Cool Reading

There was more positive news as the Producer Price Index (PPI), which measures inflation on the wholesale level, was also lower than expected in July. Headline PPI rose 0.1% last month, with the annual reading falling from 2.7% all the way down to 2.2%. Core PPI, which strips out volatile food and energy prices, was flat for the month and the year-over-year reading also saw a big drop from 3% to 2.4%.

What’s the bottom line? Wholesale inflation was much cooler than economists had forecasted, and the Bond market reacted favorably when the data was released last Tuesday. This positive trajectory lower is also important because some of the PPI components are factored into another important consumer inflation measure called Personal Consumption Expenditures (PCE), which is the Fed’s favored measure. This bodes well for a friendly PCE report when that data is released on August 30.

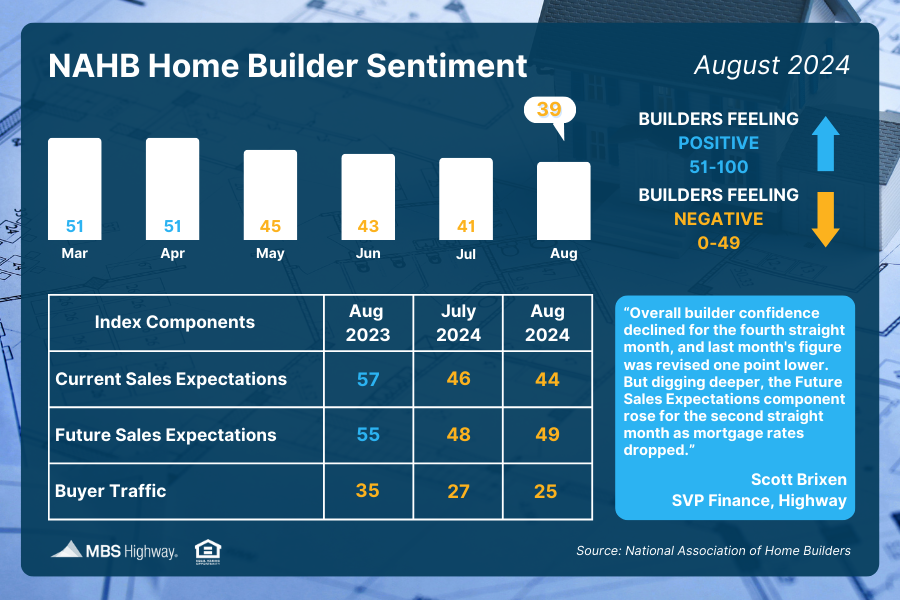

Confidence among home builders remains below the key breakeven threshold of 50, per the National Association of Home Builders (NAHB), as their Housing Market Index dropped two points to 39 in August. This marked the fourth consecutive monthly decline and the lowest reading since December as higher rates continue to dampen sentiment.

One bright spot in this report was that future sales expectations for the next six months rose by one point to 49. While still in contraction, builders expect lower interest rates will help boost demand in the next month.

Scores over 50 on this index, which runs from 0 to 100, indicate that most builders feel confident about the current and near-term housing market outlook, whereas lower readings signify there’s less optimism among builders.

What’s the bottom line? Though all three index components (buyer traffic, current and future sales expectations) remained below 50, NAHB Chief Economist, Robert Dietz, noted that, “With current inflation data pointing to interest rate cuts from the Federal Reserve and mortgage rates down markedly in the second week of August, buyer interest and builder sentiment should improve in the months ahead.”

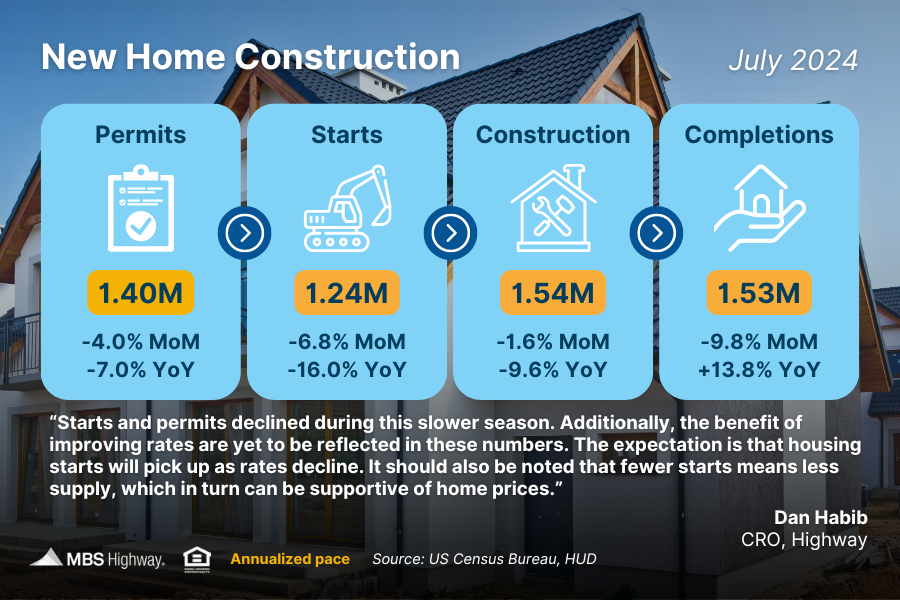

Housing Starts Slowed, Signaling a Tight Inventory Picture Ahead

Starts and Permits fell again in July, with single-family units taking the largest hit. Single-family Starts fell 14% to 850,000 units from June. This points to tighter supply for the foreseeable future, which would be supportive of higher home prices ahead.

Permits, the forward-looking indicator for new home inventory, are only at 1.4 million, which is down 4% from the previous month; showing that there are not many new homes in the pipeline. There has also been a greater fallout of permits to starts than normal, meaning that not all these permits are going to turn into new construction.

What’s the bottom line? Softer than expected construction activity could limit much needed supply down the road, especially among single-family homes. This bodes well for appreciation and shows that opportunities remain to build wealth through homeownership.

Retail Sales Hotter for the Summer

Retail Sales rose 1% in July, above the 0.3% increase the market was expecting. Sales in June were downwardly revised from 0% to -0.2%, which slightly tempers the July gain. The Core reading, which gets plugged into GDP, rose 0.3%, which was 0.2% above estimates. Sequentially, it has moderated from a 0.9% increase in June but this was also a beat and may lead to some higher GDP estimates.

What’s the bottom line? This Retail Sales release marks another report where the Core reading came in above estimates, which may lead to stronger GDP estimates down the line.

Jobless Claims Dip Lower

Initial Jobless Claims fell 7,000 in the latest week, with 227,000 people filing for unemployment benefits for the first time. Continuing Claims fell by 7,000, as 1.864 million people are continuing to receive benefits after filing their initial claim.

What’s the bottom line? Though both Initial and Continuing Claims fell last week, Continuing Claims are backing off the highest level in almost three years. This shows that once laid off, it’s harder to get back to work.

Family Hack of the Week

August 24 is National Waffle Day, and this recipe courtesy of the Food Network makes for a delicious breakfast treat. Yields 8 waffles.

Preheat waffle iron to the regular setting. In a large bowl, sift together 2 cups all-purpose flour, 1/4 cup sugar, 1 tablespoon baking powder, and 1/2 teaspoon salt. In a separate bowl, whisk together 1 1/2 cups milk, 1 tablespoon vanilla extract and 2 egg yolks. Pour the wet ingredients over the dry ingredients and stir gently until halfway combined. Melt 1 stick of salted butter and pour into mixture; continue mixing until combined.

Beat 4 egg whites until stiff and slowly fold them into the batter. Add batter to waffle iron and cook waffles in batches until they are a deep golden color and crisp. Serve immediately with butter, warm syrup and your favorite fruit topping.

What to Look for This Week

More housing reports are ahead, with July’s Existing and New Home Sales releasing on Thursday and Friday, respectively. The latest Jobless Claims will also be important to monitor on Thursday.

Look for the Fed to make headlines when the minutes from their July meeting are released on Wednesday. Investors will also be watching closely as economists, central bankers and policy makers from around the world join the Fed for its Jackson Hole Economic Symposium, which starts on Thursday.

Technical Picture

Mortgage Bonds moved higher after holding at support at 100.35 and have a lot of room to the upside until reaching resistance at 101.18.

The 10-year Treasury tested resistance at 3.92%, which held, and yields have headed lower once again. There is a lot of room for yields to improve until reaching support at 3.66%.