When it comes to getting a mortgage, there’s no shortage of misinformation. Many homebuyers, especially…

Week of June 10, 2024 in Review

Week of June 10, 2024 in Review

The Fed once again held rates steady, while tamer than expected consumer and wholesale inflation for May was a welcome sign. Unemployment claims also saw a big move higher. Here are last week’s highlights:

- Fed Holds Rates Steady, Indicates One Cut in 2024

- Consumer Inflation Takes Important Steps Lower

- Friendly Wholesale Inflation Numbers

- Initial Jobless Claims Hit 10-Month High

- Latest on Small Business Optimism

Fed Holds Rates Steady, Indicates One Cut in 2024

After eleven rate hikes since March 2022, the Fed once again left their benchmark Federal Funds Rate unchanged at a range of 5.25% to 5.5%. This decision was unanimous and marks the seventh straight meeting they held rates steady.

The Fed Funds Rate is the interest rate for overnight borrowing for banks and it is not the same as mortgage rates. The Fed has been aggressively hiking the Fed Funds Rate throughout this cycle to try to slow the economy and curb the runaway inflation that became rampant over the last few years.

What’s the bottom line? While inflation has cooled considerably after peaking in 2022, it remains above the Fed’s 2% target. Fed Chair Jerome Powell reiterated that the Fed does not expect to cut rates until members are confident that inflation is moving sustainably towards 2% as measured by annual Core Personal Consumption Expenditures (which is at 2.8% as of April).

The Fed’s “dot plot” of member forecasts signaled that just one rate cut is expected before the end of the year, down from three cuts forecasted in March, though these estimates can change quickly based on upcoming data. The Fed did acknowledge that they have seen “modest further progress” toward their 2% goal, reflecting some recent friendly inflation readings as noted below.

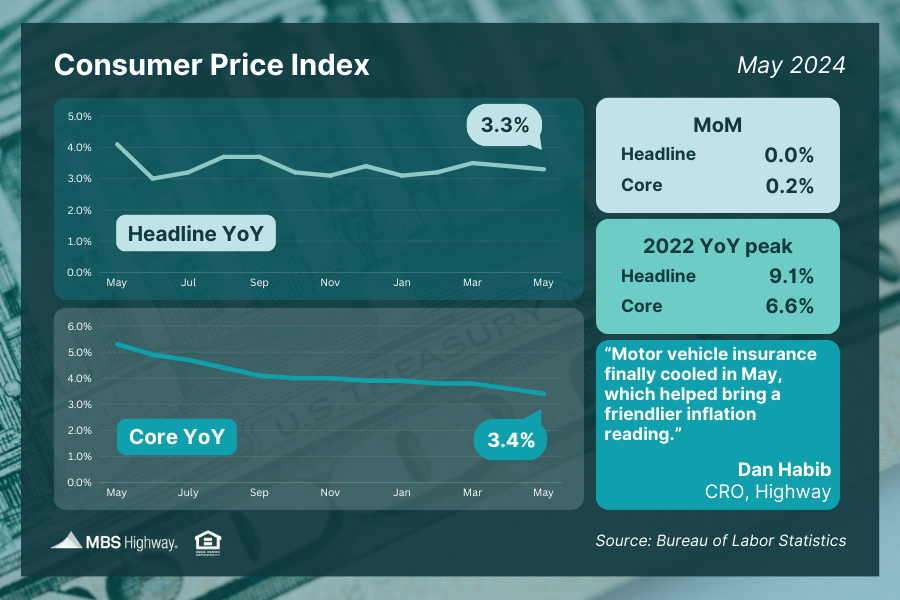

Consumer Inflation Takes Important Steps Lower

May’s Consumer Price Index (CPI) showed cooler than expected inflation, with the headline reading flat for the month while the annual reading declined from 3.4% to 3.3%. The Core measure, which strips out volatile food and energy prices, increased 0.2% and the annual reading declined from 3.6% to 3.4%.

All these measures were softer than estimates, as moderating motor vehicle insurance costs were a key reason for the friendly Core number.

What’s the bottom line? May’s data followed better than expected numbers in April. This is a welcome sign that inflationary pressures may continue to ease as we move further into the year, especially after readings in the first quarter of this year were unexpectedly high.

Friendly Wholesale Inflation Numbers

The Producer Price Index (PPI), which measures inflation on the wholesale level, was also below estimates last month. Headline PPI fell 0.2% in May, with the annual reading also moving lower from 2.3% to 2.2%. Core PPI, which strips out volatile food and energy prices, was flat in May and the year-over-year reading fell from 2.4% to 2.3%.

What’s the bottom line? The favorable CPI and PPI reports brought a double dose of positive inflation news last week. Plus, some of the PPI components are factored into another important consumer inflation measure called Personal Consumption Expenditures (PCE), which is the Fed’s favored measure, and this could lead to a friendly PCE report when that data is released on June 28.

Initial Jobless Claims Hit 10-Month High

Initial Jobless Claims rose by 13,000 in the latest week, with 242,000 people filing new unemployment claims. This was much higher than expectations of 225,000. There were also 1.82 million people still receiving benefits after filing their initial claim, as Continuing Claims jumped by 30,000.

What’s the bottom line? Initial Jobless Claims have now risen for three straight weeks, with the latest reading the highest number of first-time filers since last August. Continuing Claims are also still trending near some of the hottest levels we’ve seen in recent years, suggesting that the pace of hiring has slowed.

The Fed will be closely watching for signs of a sustained rise in unemployment as they weigh monetary policy and the timing for rate cuts, given their dual mandate and price stability and maximum employment.

Latest on Small Business Optimism

The National Federation of Independent Business (NFIB) Small Business Optimism Index rose to 90.5 in May. While this is the highest reading of the year, it remains well below the historical average of 98.

What’s the bottom line? NFIB’s Chief Economist, Bill Dunkelberg, explained that “for 29 consecutive months, small business owners have expressed historically low optimism and their views about future business conditions are at the worst levels seen in 50 years.”

Given that 22% of owners reported that inflation was the single most important problem in operating their business, the cooler than expected inflation readings for May were a positive development.

Family Hack of the Week

This easy and delicious Cherry Tart courtesy of the Food Network is perfect for marking National Cherry Tart Day on June 18. Yields 1 9-inch tart.

Preheat oven to 350 degrees Fahrenheit. To make the crust, mix 1 cup flour, 1/4 cup sugar, and 1/2 teaspoon salt in a large bowl. Add 1/2 cup butter, cut into small pieces, and pinch with fingers to create a crumb texture. Make a well in the middle and add 2 egg yolks. Quickly work in the flour mixture to create a dough; do not overmix.

Pat into a disc and refrigerate for 15 minutes, then roll dough and add to a tart pan with a removeable bottom.

To make the filling, arrange 2 cups cherries (around 50 cherries, pits removed) in the crust. Beat 3 eggs with 1/3 cup sugar, then stir in 3/4 cup crème fraiche or sour cream and 1/2 teaspoon vanilla. Pour the custard over the cherries and bake until set, around 25 minutes. Cool before serving.

What to Look for This Week

Housing data is plentiful, starting Wednesday with an update on home builder sentiment for this month. Look for May’s Housing Starts and Building Permits on Thursday, while Existing Home Sales data follows on Friday.

Also of note, May’s Retail Sales will be reported on Tuesday and the latest Jobless Claims on Thursday. Plus, we’ll see an update on manufacturing for the New York region on Monday and the Philadelphia region on Thursday.

The markets will also be closed on Wednesday for the Juneteenth holiday.

Technical Picture

Last week’s friendly inflation figures boosted Mortgage Bonds. They ended the week trading in a wide range between support at the 100-day Moving Average and overhead resistance at 100.872, which has so far prevented Bonds from making further progress higher. The 10-year is also in a wide range between support at 4.18% and overhead resistance at the 200-day Moving Average.

Related Posts